Most people pay income tax every month through PAYE without ever really understanding how the system works. That is fine until your circumstances change, a pay rise pushes you into a higher band, or you start a side income and suddenly need to think about Self Assessment. Understanding the basics makes every tax decision easier, from pension contributions to whether to take that promotion.

This guide explains how UK income tax actually works in the 2025/26 tax year, including the personal allowance, the four tax bands, and the quirky 60% effective rate that catches out high earners between £100,000 and £125,140. The rates here apply to England, Wales and Northern Ireland. Scotland has its own bands, which we cover briefly at the end.

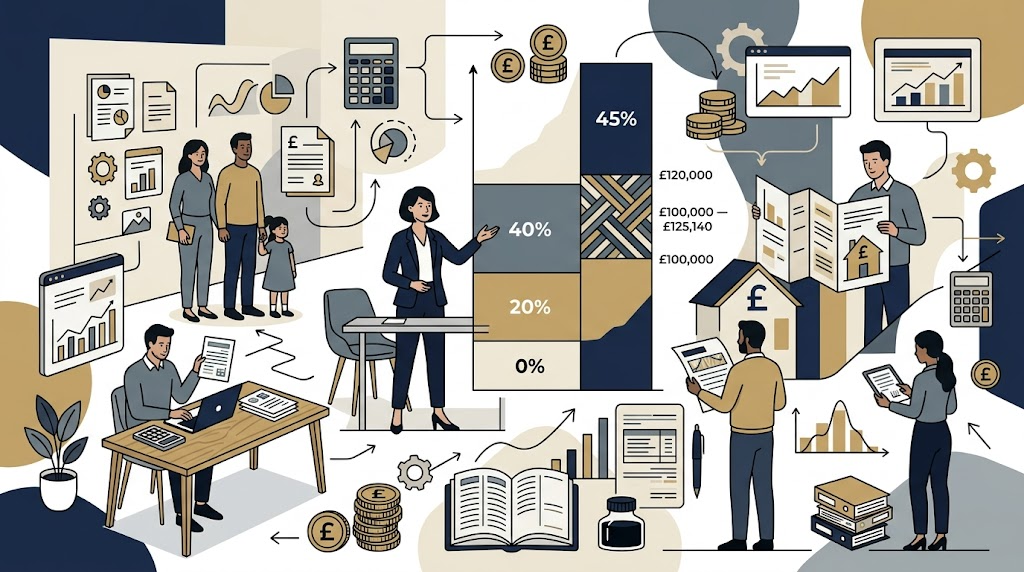

Quick Answer: UK Income Tax Bands for 2025/26

For England, Wales and Northern Ireland, income tax is paid at these rates:

- £0 to £12,570: Personal Allowance, no tax

- £12,570 to £50,270: Basic rate, 20%

- £50,270 to £100,000: Higher rate, 40%

- £100,000 to £125,140: Higher rate plus the personal allowance taper, effectively 60%

- Over £125,140: Additional rate, 45%

Each rate only applies to the income within that band, never to your whole salary.

The Personal Allowance: Your First £12,570 Is Tax-Free

Almost everyone gets a personal allowance. It is the amount you can earn each year before paying any income tax. For 2025/26 the standard personal allowance is £12,570 and it has been frozen at this level since April 2021.

The personal allowance applies to your total income, not just your salary. That includes:

- Wages from employment

- Self-employment profits

- Pension income

- Taxable interest on savings above the Personal Savings Allowance

- Rental profits

If your total taxable income is below £12,570 you owe no income tax. Above that, the next pound you earn is taxed, but only the portion above the allowance.

The Basic Rate: 20% on Income from £12,570 to £50,270

Once you go above the personal allowance, you pay 20% on every pound up to £50,270. This is the band most UK taxpayers sit in.

A practical example. If you earn £25,000 in the 2025/26 tax year:

- The first £12,570 is tax-free

- The next £12,430 is taxed at 20%, which is £2,486

- Total income tax: £2,486

Note this is income tax only. National Insurance is a separate charge and is dealt with briefly later in this guide.

The Higher Rate: 40% on Income from £50,270 to £100,000

If your taxable income goes above £50,270, anything above that threshold is taxed at 40% up to £100,000. The personal allowance and basic rate band still apply to the income below those thresholds, so you do not suddenly pay 40% on the whole salary.

Take someone earning £60,000:

- First £12,570 tax-free

- Next £37,700 at 20% (£7,540)

- Final £9,730 at 40% (£3,892)

- Total income tax: £11,432

This band catches a lot of people. Pay rises, bonuses, dividend income, and rental profits can all push higher-rate taxpayers further into this bracket without them realising.

The 60% Trap: £100,000 to £125,140

This is where how income tax works gets quirky. Once your taxable income passes £100,000, you start to lose your personal allowance. For every £2 of income above £100,000, you lose £1 of allowance. By the time you reach £125,140 the allowance is fully gone.

The effect is brutal. On income between £100,000 and £125,140, you pay 40% income tax on that band and* you pay an additional 20% on the lost allowance, because that lost allowance is now taxable too. The combined effective rate is *60%.

In real terms: every extra £1 you earn between £100,000 and £125,140 leaves you with just 40p in your pocket, before National Insurance.

This is why pension contributions and salary sacrifice arrangements are so valuable for people earning in this band. Reducing your taxable income below £100,000 restores the personal allowance and pulls you out of the 60% effective rate. It is one of the most efficient pieces of tax planning available to anyone in this income bracket.

The Additional Rate: 45% on Income Over £125,140

Once your taxable income passes £125,140, you have lost your personal allowance entirely. From this point upwards, every pound earned is taxed at 45%, the additional rate. So someone earning £150,000 keeps just 55p of every pound earned above £125,140, again before National Insurance.

The £125,140 threshold was lowered from £150,000 in April 2023 and has not moved since, pulling more high earners into the additional rate band each year.

“If I Earn More, Will I Take Home Less?” The Myth Explained

This is one of the most common tax misconceptions. People hear about crossing a tax threshold and assume the higher rate applies to their entire salary, leading some to refuse pay rises.

It does not work that way. Each rate only applies to the income within its band. If you cross from the basic rate to the higher rate by earning an extra £1, only that £1 is taxed at 40%, not the £50,271 below it.

The only exception is the 60% trap between £100,000 and £125,140, and even there you take home more than before, just less of the increase than you might have hoped.

In short: earning more always means taking home more. Always.

Fiscal Drag: The Stealth Tax Most People Miss

There has been no headline rise in UK income tax rates for several years. But total income tax revenue has gone up significantly. The reason is something called fiscal drag.

Fiscal drag happens when the government freezes tax thresholds while inflation pushes wages up. As your wages rise to keep up with prices, more of your income drifts above frozen thresholds and into higher tax bands, even though your spending power has not increased in real terms.

The personal allowance has been frozen at £12,570 since April 2021. The higher-rate threshold has been frozen at £50,270 since the same date. Both freezes are currently planned to last until April 2028.

Fiscal drag is now the single biggest contributor to rising income tax revenue, and it affects every taxpayer, especially those nudging towards a threshold each year.

A Note on Scotland

Scotland sets its own income tax bands for non-savings, non-dividend income. The principle is the same (rates only apply to the income within a band), but Scotland has six tax bands instead of three, and the rates and thresholds differ. If you live in Scotland, you pay Scottish income tax regardless of where your employer is based.

Savings income and dividend income are still taxed at UK-wide rates, even for Scottish taxpayers.

A Quick Word on National Insurance

National Insurance (NI) is a separate charge but it works similarly to income tax in many ways. Employees pay Class 1 NI on earnings above £12,570 a year, at 8% up to £50,270 and 2% above that. Self-employed people pay different classes of NI. NI is effectively a second income tax in everything but name, and it stacks on top of the income tax rates set out above.

What to Do If Your Tax Does Not Look Right

If your tax code looks wrong, your PAYE deductions seem too high, or you have crossed into a higher band and want to plan around it, a tax specialist can help. Common situations where professional advice pays off:

- You are approaching or in the 60% effective rate band (£100,000 to £125,140)

- You have multiple income sources and your tax code is not pulling everything in correctly

- You have moved between employment and self-employment

- You think you have been overpaying tax via PAYE

- You want to plan pension or salary sacrifice contributions tax-efficiently

A short review of your position can pay for itself many times over.

FAQs

How much can I earn before paying any income tax in 2025/26?

You can earn up to £12,570 before paying any income tax, assuming you receive the standard personal allowance. This is your total income across all sources, including employment, pensions, and taxable savings interest.

When does my personal allowance start to reduce?

Your personal allowance starts to reduce once your total taxable income exceeds £100,000. You lose £1 of allowance for every £2 of income above £100,000, with the allowance gone completely at £125,140.

Does the higher tax rate apply to my whole salary?

No. The higher rate only applies to the portion of your income above £50,270. Income below that threshold is still taxed at 20% (basic rate) or 0% (personal allowance).

What is fiscal drag and how does it affect me?

Fiscal drag is the effect of frozen tax thresholds combined with rising wages. As your salary increases with inflation, more of your income drifts into higher tax bands, even though your real spending power has not gone up. Most UK taxpayers are paying more in tax now than they were five years ago purely because of fiscal drag.

Should I avoid earning more to stay in a lower tax band?

No. Earning more always means taking home more, even when you cross a threshold. The higher rate only applies to income within that band, never to your whole salary. The only exception is the 60% effective rate between £100,000 and £125,140, where pension contributions can be very tax-efficient.

Are tax bands the same throughout the UK?

No. England, Wales and Northern Ireland share the same income tax bands. Scotland sets its own bands and rates for non-savings income, with six tax bands rather than three. Savings and dividend income still follow UK-wide rates everywhere.

Get Expert Income Tax Advice in Kent

Kent Tax Specialists is an ACCA and ATT qualified, HMRC Registered Agent practice with over 25 years’ personal tax experience. We help individuals across Gravesend, Dartford, Maidstone, Medway, Sevenoaks, Tonbridge, Tunbridge Wells, Canterbury and the wider Kent area with PAYE reviews, Self Assessment, tax code corrections, and planning to stay out of the 60% effective rate trap. Get in touch today for honest advice and a fixed-fee quote.

Also see: How to Check If You Have Overpaid Tax Through PAYE | What Is the High Income Child Benefit Charge? | Personal Tax services in Kent